There’s a weird thing about probability. People use it constantly but pretend they don’t.

Someone says, “There’s no way fuel prices stay this low next month.” Another person insists their team is definitely winning on Sunday. Your aunt somehow predicts rain better than weather apps just by looking outside for fifteen seconds from the balcony. Nairobi estates have at least one person like that.

Most of this is informal forecasting. Human beings are always estimating what might happen next, even casually. Prediction markets just turn those guesses into numbers people can track.

That’s basically the foundation of probability in prediction markets. Markets try to estimate how likely something is to happen using collective expectations from lots of different participants. Not certainty. Just likelihood.

Important distinction. People blur those together constantly.

Table of Contents

What Probability Actually Means

If a prediction market says there’s a 70% chance of an event happening, it does not mean the event is guaranteed.

It means the market currently believes the event is more likely than not.

That sounds obvious written down like this. Still, people struggle with it. Especially after unexpected outcomes happen and everybody suddenly claims the forecast was “wrong.”

Take weather forecasts.

If there’s a 30% chance of rain tomorrow and it rains anyway, the forecast was not necessarily inaccurate. A 30% probability still allows rain to happen sometimes. That’s the whole point of probabilities. They describe uncertainty, not certainty.

Prediction markets work the same way.

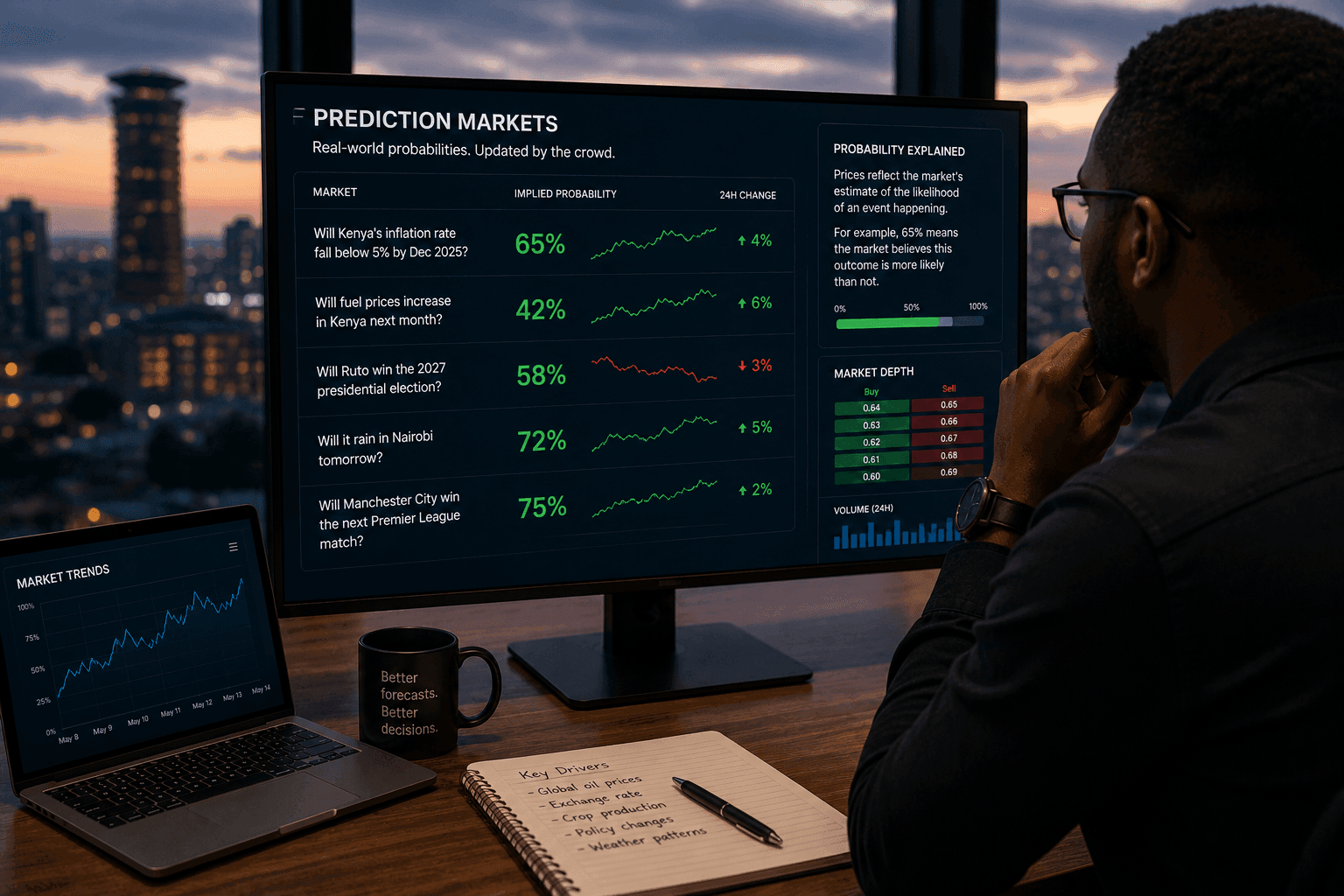

A market might estimate:

- 65% chance inflation drops later this year

- 40% chance fuel prices rise next month

- 72% chance a football team wins a match

None of these outcomes are guaranteed. They’re estimates based on current information.

People sometimes want forecasts to sound absolute because uncertainty feels annoying. Especially when money is involved. Or politics. Or football. Football discussions in Kenya become emotionally unstable very quickly honestly.

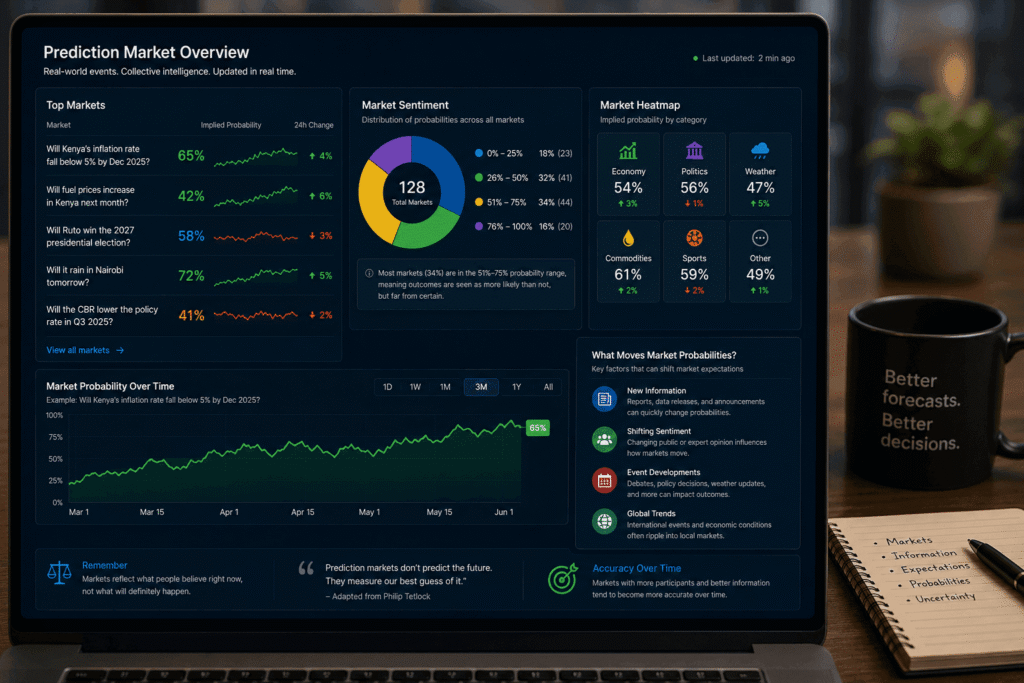

Where These Market Probabilities Come From

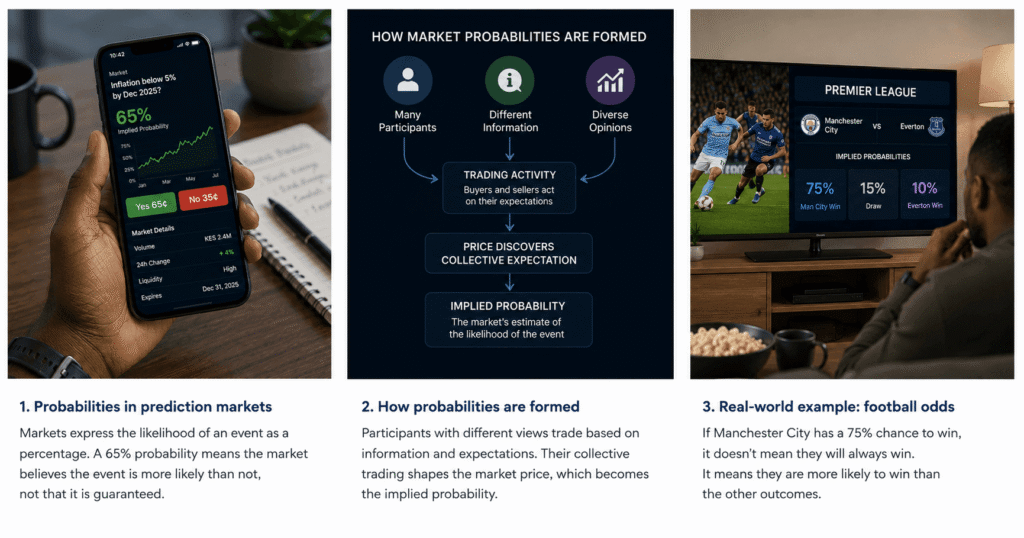

The probabilities don’t appear magically from a computer somewhere deciding the future. Markets move because participants react to information.

Someone believes inflation pressures are easing. Another trader thinks food prices will remain stubbornly high. Somebody else is watching global oil markets at midnight for reasons that probably affect their sleep schedule badly.

All these views push prices around.

As people buy or sell based on their expectations, the market adjusts. Over time the price starts reflecting the crowd’s collective estimate of probability.

That’s why forecasting markets are often described as information aggregation systems. Slightly academic phrase. But the idea is simple enough.

Different people know different things.

One participant understands election polling. Another follows central bank policy. Another tracks agricultural output or shipping costs or exchange-rate pressure. The market absorbs all this scattered information and compresses it into a probability estimate.

Not perfectly obviously. Markets can misread situations badly sometimes. Humans remain involved.

Implied Probability Explained

This is the part where articles usually become overly technical and start sounding like accounting textbooks. We’ll avoid that.

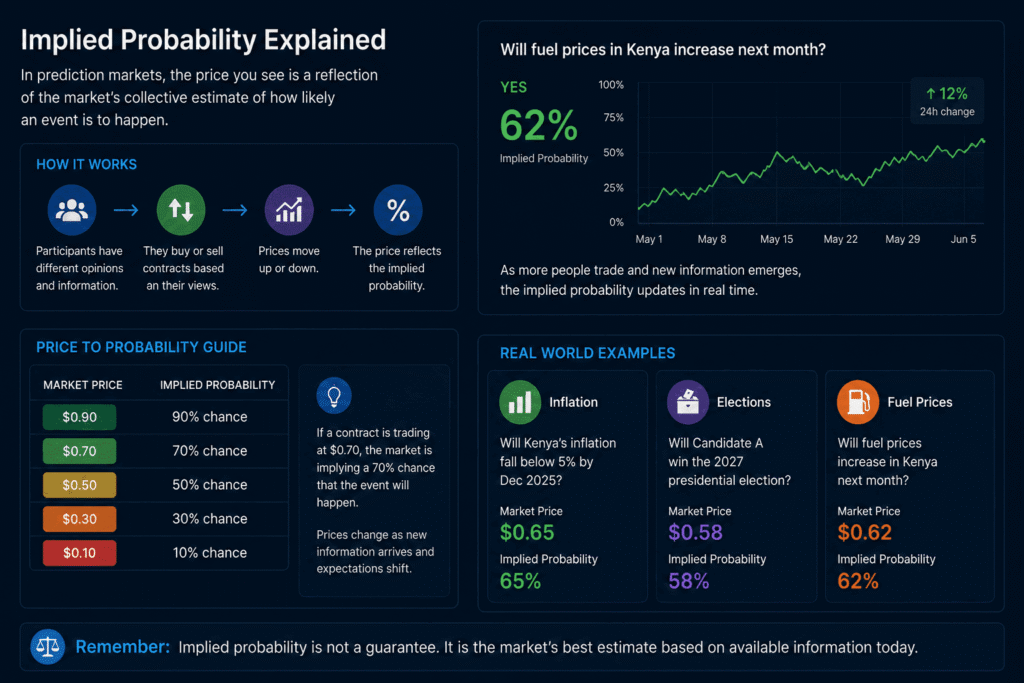

Implied probability explained simply: it’s the probability suggested by the current market price.

In many prediction markets:

- a contract trading at 80 cents implies roughly an 80% probability,

- 35 cents implies about 35%,

- and so on.

The market price becomes shorthand for collective expectation.

So imagine there’s a forecasting market asking:

Will fuel prices increase next month?

If global oil prices suddenly jump overnight, traders may think fuel price increases are now more likely. More people buy contracts tied to that outcome. The market price rises.

Maybe from 45% to 60%.

That movement reflects changing expectations based on new information.

It’s honestly not that different from how financial markets react to news generally. Currency markets do it. Bond markets do it. Even ordinary people do it informally while arguing in WhatsApp groups after Treasury announcements.

Some discussions there become very confident for no reason.

Football Is Actually a Useful Example

Football is probably the easiest shortcut for understanding forecasting probabilities because most people already understand odds instinctively.

If Manchester City plays a struggling team and the implied probability of a City win is 75%, nobody interprets that as certainty. Upsets happen constantly.

That’s why people enjoy sports in the first place. If outcomes were guaranteed, football would become unbearably boring by halftime.

Prediction markets use similar probability logic, except usually focused on broader real-world events.

For example:

- Election outcomes

- Inflation trends

- Rainfall expectations

- Commodity prices

- Central bank decisions

The structure changes, but the underlying probability idea stays mostly the same.

An event with 70% implied probability should happen more often than an event sitting at 20%. Not always. Just over time.

Humans are surprisingly uncomfortable with “probably.” We prefer certainty even when reality clearly doesn’t operate that way.

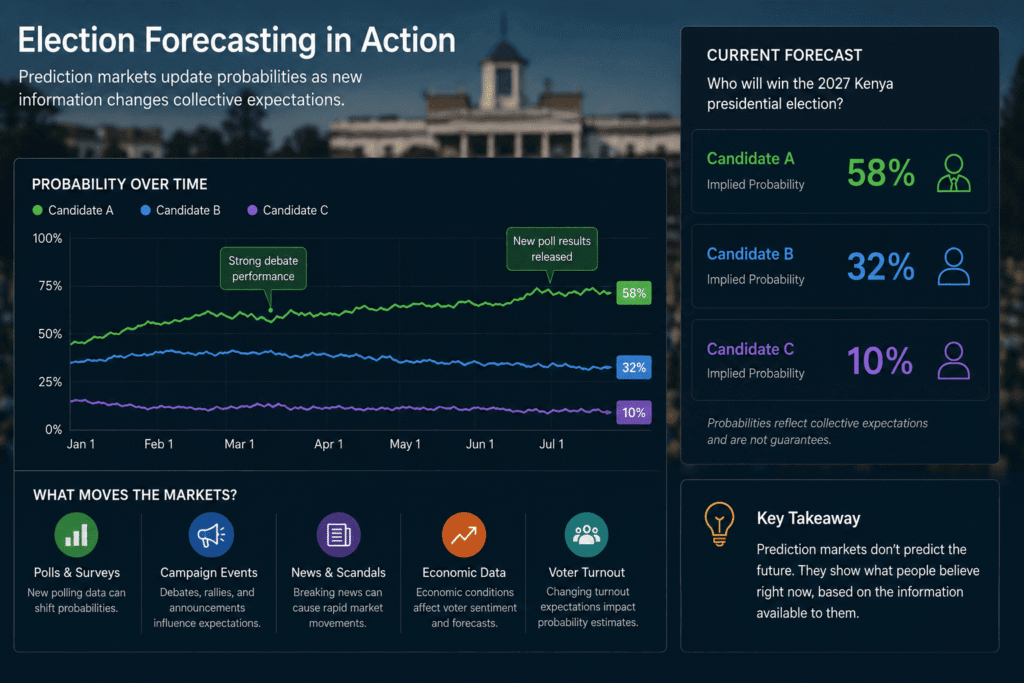

Election Forecasts Make This Easier to Visualize

Election forecasting markets are useful examples because probabilities move visibly as information changes.

Suppose a market estimates:

- Candidate A: 58%

- Candidate B: 42%

That doesn’t mean Candidate A has already won. It means the market currently believes Candidate A is somewhat more likely to win based on available evidence.

The evidence could include:

- polling,

- campaign momentum,

- economic conditions,

- turnout expectations,

- media coverage,

- regional voting patterns,

- fundraising activity.

Then new information arrives and probabilities shift.

A debate goes badly. Economic data changes public sentiment. A coalition forms unexpectedly. Suddenly the market adjusts from 58% down to 49%.

Forecasting markets behave dynamically because expectations change dynamically.

Which honestly feels more realistic than pretending forecasts should remain fixed while the world keeps moving around underneath them.

Why Forecasting Probabilities Matter

Forecasting probabilities help because they force people to think more precisely about uncertainty.

Normally conversations stay vague.

People say:

- “probably”

- “unlikely”

- “almost certain”

- “good chance”

Those phrases mean different things depending on who’s talking.

One person hears “likely” and thinks 55%. Another imagines 90%.

Markets force participants to translate vague feelings into measurable estimates.

That makes it easier to track changing expectations over time.

For example:

- drought probability rising from 20% to 50% is meaningful,

- inflation expectations falling sharply matters,

- election odds narrowing quickly tells analysts something important is changing.

These probability shifts become informational signals.

Researchers, investors, journalists, and policymakers often watch these movements because markets sometimes detect changes earlier than conventional commentary does.

Not always. But often enough that people pay attention.

Markets Reflect Expectations, Not Truth

This part gets missed constantly online.

Prediction markets do not reveal objective truth. They reflect collective expectations at a specific moment in time.

That means markets can become overly emotional or temporarily irrational too.

Political markets may overreact to breaking headlines. Economic markets sometimes become too optimistic during booms and too pessimistic during downturns. Public mood affects pricing more than people admit.

Crowds are intelligent in aggregate surprisingly often. But crowds are still made of humans refreshing apps at 1 a.m. while tired and emotional and maybe overconfident after reading three charts.

So market probabilities should be interpreted carefully.

They’re useful forecasting tools. Not crystal balls.

Probability Is Really About Managing Uncertainty

At the center of all this is one uncomfortable reality: uncertainty never disappears completely.

Prediction markets don’t eliminate uncertainty. They organize it.

That’s the important shift.

Instead of asking:

“What will definitely happen?”

Forecasting systems ask:

“What outcome currently appears most likely given available information?”

That approach sounds less dramatic. Less emotionally satisfying too maybe. But it tends to produce better analysis over time.

And honestly the world already has enough fake certainty floating around. Especially online. Every week somebody confidently predicts an economic collapse or a guaranteed election landslide and then quietly disappears when reality becomes inconvenient.

Probability-based forecasting at least admits the future is messy before trying to estimate it anyway.