There’s a funny thing that happens whenever prediction markets come up in conversation in Kenya. Someone usually says, “So basically betting?” Then another person says something about Aviator or Premier League accumulators and the discussion drifts off into odds and last-minute goals. It happens a lot. Probably because both systems involve uncertainty, probabilities, and people risking money on outcomes. From a distance, they can look similar enough.

But prediction markets and traditional betting actually work very differently underneath. The incentives are different. The purpose is different. Even the way information moves through the system is different. And that distinction matters more now than it did a few years ago, partly because forecasting markets are starting to show up in discussions around elections, inflation, policy expectations, commodity prices, and business decisions. Not just sports.

The confusion is understandable though. Humans like categories. If money is involved and the future is uncertain, people throw it all into the “gambling” bucket. Sometimes unfairly. Nairobi has a habit of flattening complicated things into simple labels anyway. Someone once called treasury bills “government betting.” Which was not correct, but weirdly confident.

Table of Contents

The Core Difference: Forecasting vs Gambling

The easiest way to explain prediction markets vs betting is this:

Traditional betting is mainly entertainment built around risk.

Prediction markets are systems designed to aggregate information about future events.

That sounds abstract at first, but it changes almost everything.

In sports betting, odds are usually set by a bookmaker. The bookmaker’s job is not really to discover truth. Their job is to balance exposure, manage risk, and ensure profit margins over time. Odds move partly because of information, but also because of betting volume and liability management.

Prediction markets work differently. Prices move because participants collectively express beliefs about probability. A market price of 70% generally means participants think there is roughly a 70% chance an event happens. That probability interpretation is central.

So if a forecasting market says there’s a 65% chance Kenya’s inflation rate falls below a certain threshold next quarter, the market is functioning more like a live consensus estimate than a sportsbook line.

Not a perfect estimate, obviously. Markets can be wrong. Often dramatically wrong. Financial markets misread Brexit. Analysts misread inflation after COVID. Polls missed things too. But the mechanism is designed around information discovery rather than entertainment spending.

That’s the important split in the forecasting vs gambling conversation.

How Information Gets Processed

Prediction markets rely heavily on information aggregation. That phrase sounds academic because it is academic. But the idea itself is pretty normal.

Different people hold different pieces of information. One trader follows central bank policy closely. Another tracks fuel prices. Someone else watches shipping data or weather patterns affecting agriculture. Individually, nobody sees the whole picture. Together, markets can combine those fragments into a probability estimate.

Economists have studied this for decades. In many cases, prediction markets have performed surprisingly well at forecasting elections, policy outcomes, and even disease spread. Not perfectly. Just consistently useful.

Sports betting markets also process information, to be fair. Premier League odds reflect injuries, team form, travel schedules, weather, and public sentiment. But the structure is still entertainment-first. Nobody seriously argues that betting odds are primarily tools for public policy analysis. Though football fans in Kenya sometimes treat them like macroeconomic indicators after a bad weekend.

Prediction markets increasingly get used in areas where organizations actually want better forecasts.

A government agency might want probability estimates on drought conditions. A newsroom could track election likelihoods. A company may forecast supply-chain disruption. Investors may monitor recession expectations.

The market becomes a decision-support system, not just a wagering venue.

That distinction matters more than people think.

Why Prediction Markets Often Look Less Emotional

Traditional betting is heavily emotional. By design, honestly.

Fans bet on teams they support. People chase losses. There’s adrenaline in it. Sometimes frustration. Sometimes irrational confidence after watching one good half of football. Sportsbooks know this and build products around engagement patterns.

Prediction markets tend to reward analytical thinking more directly. Participants are usually trying to estimate probabilities as accurately as possible because pricing inefficiencies create opportunity.

If a market estimates only a 20% chance of an event you strongly believe has a 50% chance of happening, there’s a potential trade there.

That changes user behavior.

The emotional side never disappears completely. Humans are still humans. Markets can become ideological or reactive, especially around politics. But forecasting systems generally encourage participants to think in percentages, expected outcomes, and information quality rather than pure excitement.

Which sounds dry until you actually spend time around people obsessed with forecasting models. Then you realize probability discussions can become strangely intense. More intense than they should be for people staring at spreadsheets at 11 p.m.

Kenyan Examples Make the Difference Easier to See

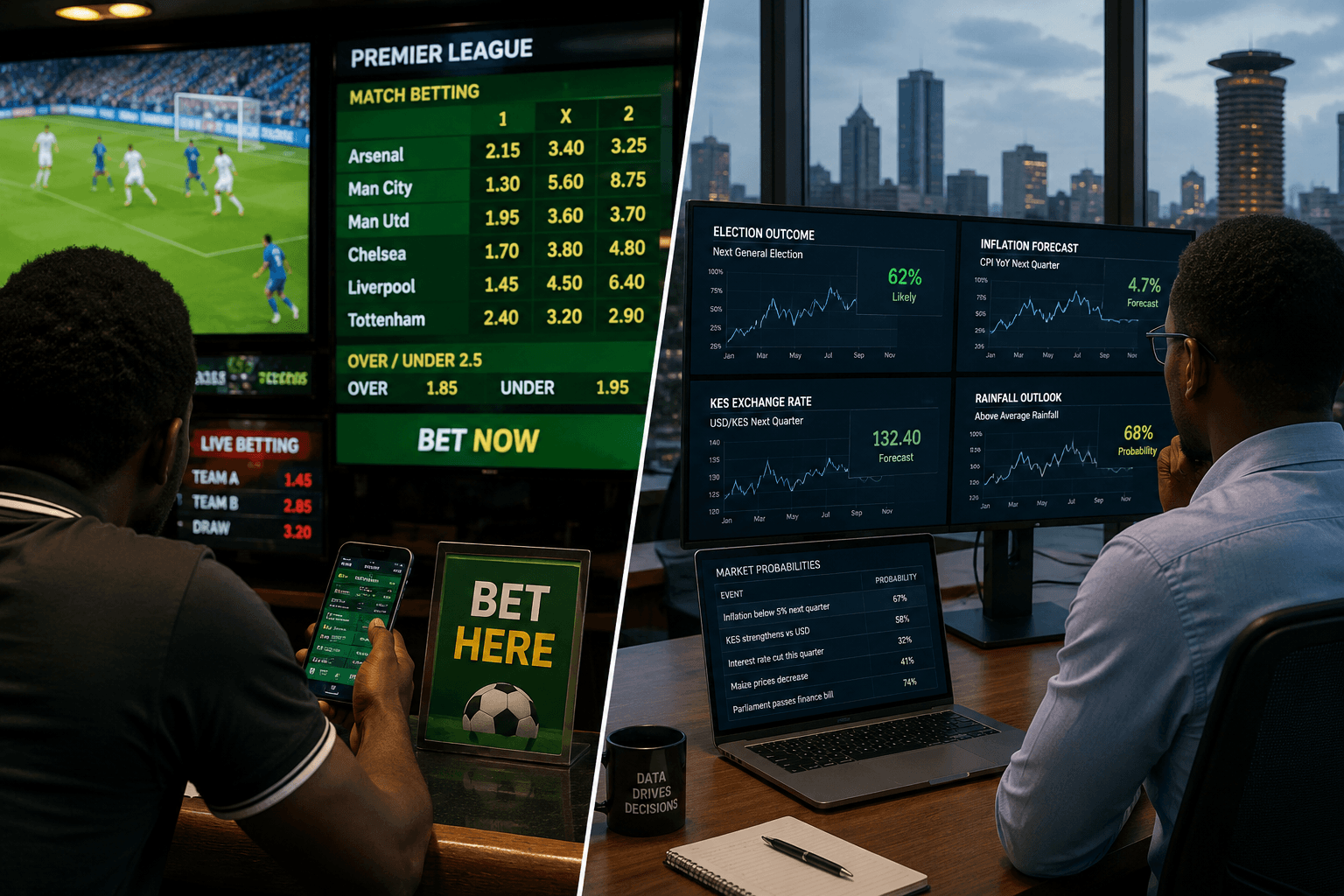

Take football betting in Kenya. Most users already understand the basic structure. You place money on Arsenal to win, or on over 2.5 goals, and the bookmaker pays according to fixed odds. The experience is direct and outcome-focused.

Now compare that with a hypothetical prediction market asking:

- Will Kenya’s inflation rate fall below 5% by December?

- Will rainfall in certain agricultural regions exceed seasonal averages?

- Will the shilling strengthen against the dollar this quarter?

- Will a major infrastructure project meet its completion target?

These are fundamentally forecasting questions. The market’s value comes from generating probability estimates that people can interpret and analyze.

A journalist might look at changing market probabilities to understand public expectations. An investor might use them alongside economic indicators. Researchers may compare market forecasts against polling or institutional projections.

Nobody is watching injury time hoping for a miracle equalizer.

Different psychology entirely.

Probability Interpretation Is a Big Deal

One overlooked aspect of prediction markets is how they force people to think probabilistically.

In normal conversation, people speak with certainty all the time.

“This will definitely happen.”

“No chance.”

“Surely prices will drop.”

Reality rarely behaves that cleanly.

Prediction markets push participants toward numerical thinking. Instead of saying an event “will happen,” users express confidence levels. Maybe 60%. Maybe 35%. Maybe 82%.

That sounds small, but it changes decision-making quality.

A policymaker interpreting a 70% probability of drought risk behaves differently than one hearing vague speculation. Businesses often make better decisions when uncertainty gets quantified instead of ignored.

This is one reason forecasting systems attract economists, analysts, political scientists, and institutional researchers. They create structured uncertainty rather than pretending uncertainty does not exist.

Which, honestly, is refreshing sometimes. Plenty of public debate in Kenya still treats prediction like a confidence competition.

The Legal and Regulatory Conversation

The topic of prediction market legality is complicated because legal systems around the world classify these platforms differently.

Some jurisdictions regulate them similarly to financial products. Others treat them closer to betting services. In certain countries, limited forms are allowed for research purposes while broader retail participation faces restrictions.

The legal distinction often depends on:

- how the market is structured,

- whether contracts are considered financial instruments,

- how payouts work,

- and whether the primary purpose is forecasting or entertainment.

That’s why conversations about prediction markets usually involve regulators, economists, legal scholars, and policy researchers — not just gaming authorities.

In Africa, regulatory frameworks are still evolving. Kenya already has a large digital betting ecosystem, so any forecasting market entering the region naturally gets compared to existing gambling structures. Some overlap exists operationally, but policymakers increasingly recognize that information markets may serve broader analytical functions.

The details matter here. A lot.

Why Organizations Care About Forecasting Markets

One reason prediction markets keep attracting attention is simple: traditional forecasting methods are often weak.

Polls can miss trends. Expert panels sometimes become groupthink exercises. Internal company forecasting gets distorted by office politics surprisingly often. Anyone who has sat through corporate quarterly planning meetings already knows this.

Prediction markets offer an alternative mechanism.

Instead of asking a few experts for opinions, organizations let many participants trade on expectations. The resulting price becomes a dynamic probability estimate that updates continuously as new information appears.

Research over the years has shown these systems can outperform conventional forecasts in some contexts, especially where dispersed information matters.

Not every time. Forecasting remains hard. There is no magic system for predicting complex social events. If there were, Nairobi traffic would already be solved and half the city wouldn’t still leave home absurdly early for meetings.

Still, the information aggregation aspect makes prediction markets valuable beyond entertainment.

That’s the key idea people miss when reducing them to “just betting.”

Betting Alternatives or Something Else Entirely?

Calling prediction markets “betting alternatives” is partially accurate but incomplete.

Yes, both involve uncertainty and financial stakes.

But prediction markets are closer to probabilistic information systems than traditional gambling products. Their social value comes less from excitement and more from collective forecasting capability.

That distinction explains why universities study them, researchers cite them, and analysts increasingly monitor them alongside polls, surveys, and economic indicators.

Over time, public understanding of prediction markets will probably become more nuanced. The same thing happened with financial derivatives, which initially looked incomprehensible to most people outside finance. Some still are, honestly.

For now, the important thing is recognizing that not every market about future events exists for the same reason.

Some are built mainly for entertainment.

Others are built to answer difficult questions about the future a little more accurately than humans usually can on their own.