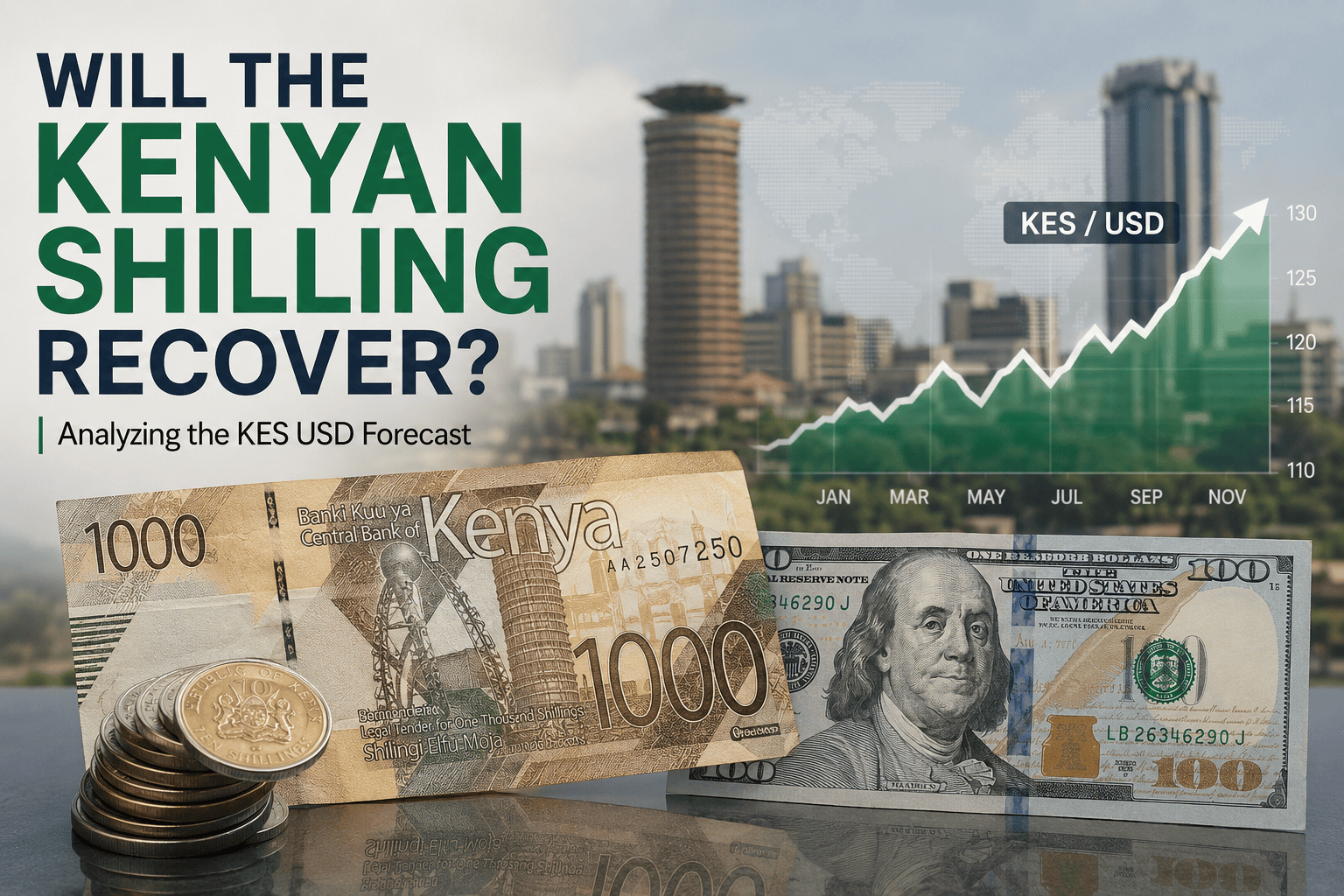

The Kenyan shilling has had an interesting few years. Not long ago, almost every conversation about the currency centered on weakness. Importers worried about rising costs. Travelers complained that foreign currency had become expensive. Businesses with dollar-denominated loans were under pressure. Then things shifted. The shilling strengthened more than many people expected, and suddenly the discussion became whether that recovery could actually last.

Currencies rarely move because of one thing. They’re more like weather systems than switches. A stronger exchange rate today doesn’t automatically mean the same trend continues next quarter. Sometimes it does. Sometimes it fades quietly.

So when people search for a KES USD forecast, they’re often hoping for a simple answer. There usually isn’t one.

Table of Contents

Why the Kenyan shilling moves

Exchange rates reflect supply and demand, but the forces behind that supply and demand can get complicated surprisingly fast.

Kenya imports fuel, machinery, pharmaceuticals, electronics, and plenty of other goods priced in US dollars. Every time businesses need dollars to pay suppliers abroad, demand for foreign currency rises.

At the same time, Kenya earns foreign exchange through exports like tea, coffee, horticulture, tourism, remittances from Kenyans living overseas, and foreign investment.

If more dollars enter the country than leave it, the shilling generally benefits. If the opposite happens for long enough, pressure builds.

It’s simple in theory. Reality is messier.

Inflation still matters

Inflation doesn’t always grab headlines unless food prices jump sharply, but it’s one of the foundations behind currency performance.

If inflation remains consistently higher than that of major trading partners, purchasing power gradually erodes. Investors often become less interested in holding assets denominated in that currency unless interest rates compensate for the difference.

Kenya has generally managed inflation better than many countries in recent years, although food prices and weather-related shocks continue to create volatility. Agriculture still plays a large role in the economy, so rainfall matters more than people outside the region sometimes realize.

One poor harvest can ripple through prices much faster than expected.

Interest rates and the Central Bank

The Central Bank of Kenya (CBK) has another important tool: monetary policy.

Higher interest rates can make Kenyan government securities more attractive to investors. That may increase demand for the shilling as foreign investors purchase local assets.

But higher rates also slow borrowing and investment inside the domestic economy. Businesses feel it. Consumers usually do too.

Finding the right balance is never straightforward. Central banks everywhere deal with this trade-off, not just in Kenya.

Foreign exchange reserves provide confidence

Foreign reserves don’t determine exchange rates by themselves, but they influence confidence.

Healthy reserves give policymakers more flexibility if foreign currency markets become volatile. Investors often pay attention to whether a country’s reserves cover several months of imports because it offers some reassurance that external obligations can still be met.

Strong reserves also reduce concerns about sudden shortages of foreign currency.

Markets notice these things, even if most people don’t spend much time thinking about reserve data over breakfast.

Trade balance remains a structural challenge

Kenya continues to import more goods than it exports.

That trade deficit creates ongoing demand for foreign currency. Even during periods when the shilling strengthens, the underlying structure of the economy doesn’t change overnight.

Exports have grown in several sectors, particularly horticulture and services, but reducing a persistent trade imbalance usually takes years rather than months.

Energy imports also matter. When global oil prices rise sharply, Kenya often needs substantially more dollars to pay fuel bills.

That alone can change the outlook.

Remittances have become increasingly important

One of Kenya’s quieter economic success stories has been the steady growth of remittances.

Money sent home by Kenyans working abroad has become one of the country’s largest sources of foreign exchange. Unlike some investment flows, remittances tend to be relatively stable even when financial markets become nervous.

That stability can provide support for the shilling during uncertain periods.

It’s probably not the first statistic people think about when discussing exchange rates, but it’s an important one.

Global economic trends cannot be ignored

The Kenyan shilling doesn’t move in isolation.

When the US dollar strengthens globally, many emerging market currencies come under pressure. This often happens when US interest rates rise or investors seek safer assets during periods of uncertainty.

Commodity prices matter too.

Oil prices influence Kenya’s import bill, while demand for tea, coffee, and horticultural exports depends partly on economic conditions in overseas markets.

Events happening thousands of kilometers away can end up influencing prices in Nairobi surprisingly quickly.

Possible scenarios for the KES USD forecast

Rather than making a single prediction, it’s more useful to think in probabilities.

Scenario 1: Continued gradual stability

If inflation remains under control, remittances stay strong, tourism performs well, and foreign exchange reserves remain healthy, the shilling could continue trading within a relatively stable range.

This doesn’t necessarily mean large gains against the US dollar. Stability itself can be valuable for businesses planning imports and investments.

Scenario 2: Moderate weakening

A rise in global oil prices, slower export growth, weaker foreign investment, or renewed dollar strength internationally could gradually push the shilling lower.

This would probably happen over time rather than through a sudden collapse, assuming broader economic conditions remain manageable.

Scenario 3: Stronger-than-expected appreciation

It’s the less discussed possibility.

If export earnings accelerate, tourism exceeds expectations, remittance inflows continue growing, and investor confidence improves simultaneously, the shilling could strengthen further against the dollar.

That would likely require several positive factors working together rather than just one.

Scenario 4: External shock

Unexpected geopolitical events, global recessions, financial crises, or major commodity price spikes could quickly change currency markets worldwide.

These risks are difficult to forecast precisely because they often emerge with little warning.

That’s why most professional currency forecasts are revised regularly.

What indicators should people watch?

Anyone following the Kenyan shilling doesn’t need to monitor every economic report released around the world.

A handful of indicators usually provides a good starting point:

- Inflation trends in Kenya

- CBK interest rate decisions

- Foreign exchange reserve levels

- Monthly remittance inflows

- Global oil prices

- Export performance

- Tourism arrivals

- US Federal Reserve policy decisions

None of these tells the whole story individually. Together, they paint a more complete picture.

The bottom line

The outlook for the Kenyan shilling depends on a combination of domestic economic management and international conditions. Inflation, interest rates, foreign reserves, remittances, trade balances, and global financial markets all play meaningful roles.

For now, the evidence supports several plausible paths rather than one certain outcome. The most reasonable KES USD forecast isn’t a fixed number but a range of possibilities shaped by incoming economic data.

That’s one of the less satisfying parts of forecasting. People naturally prefer certainty. Markets almost never provide it.

The better approach is to watch the indicators, update expectations as new information arrives, and accept that exchange rates are influenced by many moving pieces, some predictable and others not.