Table of Contents

Fuel Prices in Kenya: Will They Go Up This Month?

It’s one of those questions that comes up quietly but often — maybe at a petrol station queue, or someone scrolling on their phone after seeing global oil headlines. Are fuel prices going up again?

The short answer is: maybe. Slight bias toward an increase, but it’s not locked in. Kenya’s fuel pricing is always sitting on a few moving parts that don’t really move in sync.

And also, EPRA adjustments don’t always behave in a way that feels intuitive if you’re just watching crude oil charts.

What Actually Drives Fuel Prices in Kenya (in practice, not theory)

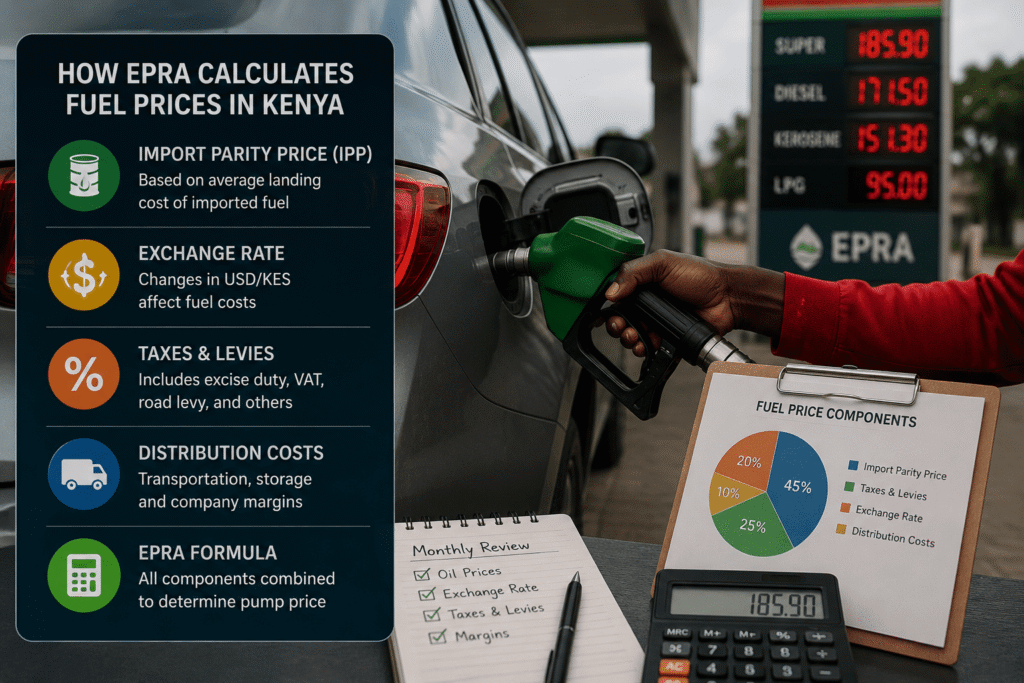

The Energy and Petroleum Regulatory Authority (EPRA) reviews fuel prices monthly, usually around the 15th. But what they’re really doing is stitching together three main inputs:

1. Global crude oil prices

Brent crude is still the reference point. When it rises, imported refined fuel tends to get more expensive. Lately, oil markets have been a bit… uneven. Not a clean trend. Some weeks up, some weeks drifting down again depending on supply expectations and geopolitical noise.

You’ll see analysts talk about OPEC decisions, shipping disruptions, demand forecasts — all of that matters, but by the time it reaches Nairobi pump prices, it’s already filtered through multiple layers.

2. USD/KES exchange rate

This one is underrated in public discussions, but very important.

Kenya imports fuel in dollars. So even if global oil prices stay flat, a weaker shilling pushes domestic fuel prices up.

The Kenyan shilling has had periods of stability recently, but also still reacts quickly to dollar demand cycles, debt payments, and import pressure. It doesn’t need to move a lot to matter.

Even a small shift like 1–3% can quietly influence the next EPRA adjustment.

3. Taxes and fixed levies

There’s also the part that doesn’t move much but still matters: taxes, transport margins, and regulatory components.

These don’t usually explain month-to-month changes, but they set a baseline that keeps prices “sticky” on the downside. So even if oil drops, pump prices don’t always fall as much as people expect.

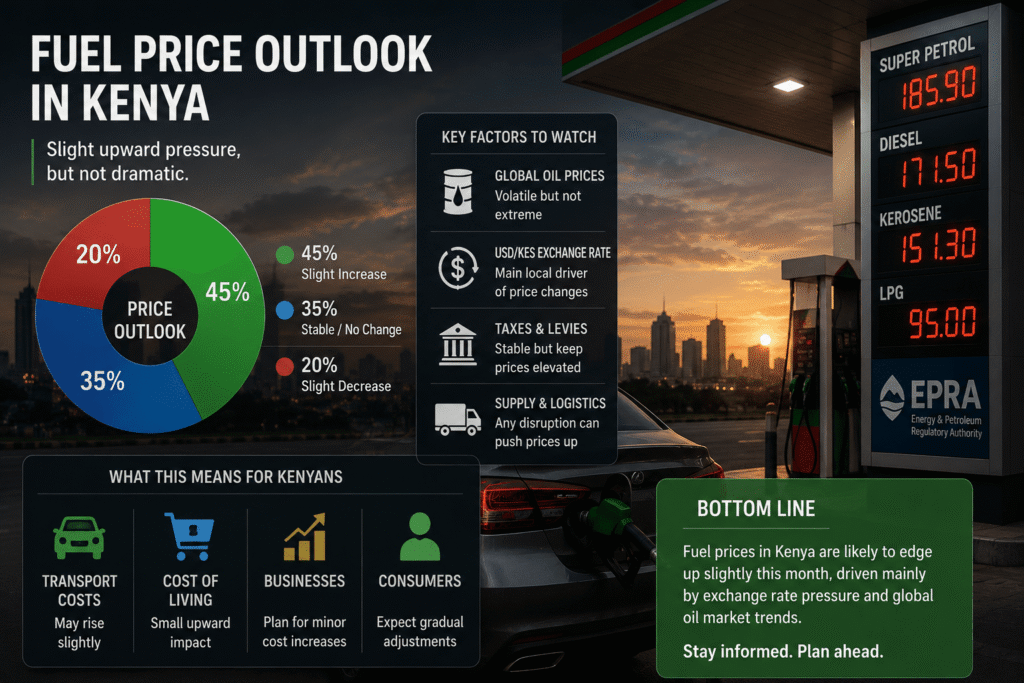

So… What’s the Direction This Month?

Based on recent patterns (and assuming no sudden external shock), here’s a rough probability framing:

- 45% chance: slight increase in fuel prices

- 35% chance: stable / minimal change

- 20% chance: small decrease

Not scientific precision. More like a structured guess based on how these inputs are behaving at the same time.

The slight upward bias comes mostly from two things:

- exchange rate pressure that hasn’t fully relaxed

- oil prices not staying consistently low long enough to force a clear downward adjustment

But it’s not a strong “prices will spike” situation either. More like mild upward drift risk.

The Weird Part: Timing Matters More Than People Think

Something that often gets missed — oil prices two weeks ago matter more than oil prices today.

EPRA’s pricing window doesn’t perfectly match real-time market sentiment. So you can have a week where global oil drops, and still see pump prices go up just because earlier averages were higher.

It creates this lag effect that feels slightly unfair, depending on when you’re paying attention.

Also, there are months where nothing obvious happens globally, and yet local prices still shift. That’s usually FX movement doing quiet work in the background.

Inflation and Consumer Pressure (the background noise)

Inflation in Kenya has cooled compared to previous peaks, but fuel is still one of those categories that feeds back into everything else — transport, food distribution, small businesses.

So even “small” fuel increases tend to have a wider ripple effect. Matatu fares adjust slowly, sometimes inconsistently. Delivery costs change quietly before anyone announces anything.

There’s also a behavioural layer here: people expect fuel to go up eventually, so expectations themselves start shaping reactions.

Not in a dramatic way. Just small adjustments in planning and pricing.

A Simple Way to Think About It

If you strip everything down:

- Oil prices = global pressure

- USD/KES = local amplification

- EPRA formula = smoothing mechanism with delay

And the result is a system that rarely moves in straight lines.

Sometimes it feels like prices should follow headlines, but they don’t. They follow averages, timing windows, and currency drift that’s easy to miss if you’re only checking once in a while.

What Would Change the Forecast Quickly?

A few triggers that could shift things fast:

- sudden jump in Brent crude (supply shock or geopolitical escalation)

- sharp weakening of the shilling against the dollar

- unexpected tax or subsidy adjustment (less common, but possible in policy shifts)

- global refinery constraints affecting refined product supply

Any one of these can override the “mild drift” scenario pretty quickly.

Final Thought (not really a conclusion)

Fuel pricing in Kenya doesn’t behave like a single-variable problem. It’s more like three or four clocks ticking at slightly different speeds.

Right now, those clocks aren’t perfectly aligned, but they’re not wildly out of sync either.

So the base case remains: slight upward pressure, but not dramatic. Unless something external breaks the pattern, it’s probably another month of small adjustments that people notice for a day, then move on from.

And then someone will still check the petrol station board twice, just to be sure.